Malaysia Personal Income Tax Relief 2022

Malaysian personal tax relief 2022. Below is the list of tax relief items for resident individual for the assessment year 2021. The relief amount you file will be deducted from your income thus reducing your taxable income. Make sure you keep all the receipts for the payments.

Tax Relief For Resident Individual for Assessment Year 2021

| No | Individual Relief Types | Amount (RM) |

|---|---|---|

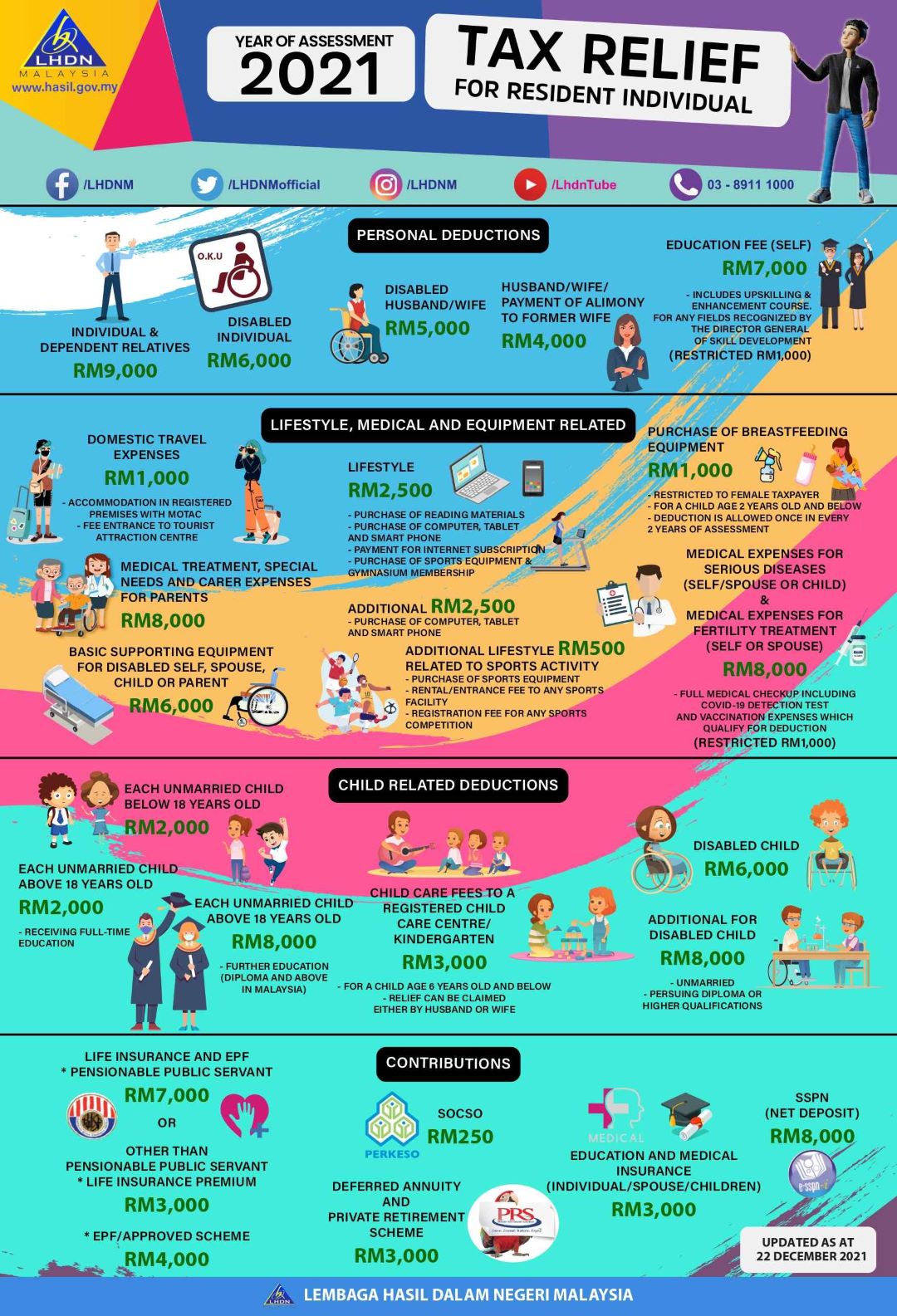

| 1 | Individual and dependent relatives | 9,000 |

| 2 | Medical treatment, special needs and carer expenses for parents (Medical condition certified by medical practitioner) | 8,000 (Restricted) |

| 3 | Purchase of basic supporting equipment for disabled self, spouse, child or parent | 6,000 (Restricted) |

| 4 | Disabled individual | 6,000 |

| 5 | Education fees (Self) Other than a degree at masters or doctorate level - Course of study in law, accounting, islamic financing, technical, vocational, industrial, scientific or technology Degree at masters or doctorate level - Any course of study Any course of study undertaken for the purpose of up-skilling or self-enhancement recognized by the Director General of Skills Development under the National Skills Development Act 2006 – effective from YA 2021 until YA 2022. (Restricted to 1,000) |

7,000 (Restricted) |

| 6 | Medical expenses for serious diseases for self, spouse or child | 8,000 (Restricted) |

| 7 | Medical expenses for fertility treatment for self or spouse | |

| 8 | Vaccination expenses for self, spouse and child. Types of vaccine which qualify for deduction are as follows: Pneumococcal; Human papillomavirus (HPV); Influenza; Rotavirus; Varicella; Meningococcal; TDAP combination ( tetanus-diphtheria-acellular-pertussis); and Coronavirus Disease 2019 (Covid-19) (Restricted to 1,000) |

|

| 9 | (i) Complete medical examination for self, spouse, child as defined by the Malaysian Medical Council (MMC). (ii) COVID-19 detection test including purchase of self detection test kit for self, spouse, child. (Restricted to 1,000) |

|

| 10 | Lifestyle – Expenses for the use / benefit of self, spouse or child in respect of: purchase and subscription of books / journals / magazines / newspapers (including electronic subscription) / other similar publications (Not banned reading materials) purchase of personal computer, smartphone or tablet (Not for business use) purchase of sports equipment for sports activity defined under the Sports Development Act 1997 and payment of gym membership payment of monthly bill for internet subscription (Under own name) |

2,500 (Restricted) |

| 11 | Lifestyle – Purchase of personal computer, smartphone or tablet for self, spouse or child and not for business use This deduction is an addition to the deduction granted under item 10. |

2,500 (Restricted) |

| 12 | Purchase of breastfeeding equipment for own use for a child aged 2 years and below (Deduction allowed once in every 2 years of assessment) | 1,000 (Restricted) |

| 13 | Payment for child care fees to a registered child care centre / kindergarten for a child aged 6 years and below | 3,000 (Restricted) |

| 14 | Net deposit in Skim Simpanan Pendidikan Nasional (Net deposit is the total deposit in 2021 MINUS total withdrawal in 2021) | 8,000 (Restricted) |

| 15 | Husband / wife / payment of alimony to former wife | 4,000 (Restricted) |

| 16 | Disabled husband / wife | 5,000 |

| 17 | Each unmarried child and under the age of 18 years old | 2,000 |

| 18 | Each unmarried child of 18 years and above who is receiving full-time education ("A-Level", certificate, matriculation or preparatory courses). | 2,000 |

| 19 | Each unmarried child of 18 years and above that: receiving further education in Malaysia in respect of an award of diploma or higher (excluding matriculation/ preparatory courses). receiving further education outside Malaysia in respect of an award of degree or its equivalent (including Master or Doctorate). the instruction and educational establishment shall be approved by the relevant government authority. |

8,000 |

| 20 | Disabled child | 6,000 |

| Additional exemption of RM8,000 disable child age 18 years old and above, not married and pursuing diplomas or above qualification in Malaysia @ bachelor degree or above outside Malaysia in program and in Higher Education Institute that is accredited by related Government authorities |

8,000 | |

| 21 | Life insurance and EPF INCLUDING not through salary deduction Pensionable public servant category Life insurance premium OTHER than pensionable public servant category Life insurance premium (Restricted to RM3,000) Contribution to EPF / approved scheme (Restricted to RM4,000) |

7,000 (Restricted) |

| 22 | Deferred Annuity and Private Retirement Scheme (PRS) - with effect from year assessment 2012 until year assessment 2025 | 3,000 (Restricted) |

| 23 | Education and medical insurance (INCLUDING not through salary deduction) | 3,000 (Restricted) |

| 24 | Contribution to the Social Security Organization (SOCSO) | 250 (Restricted) |

| 25 | Payment for accommodation at premises registered with the Commissioner of Tourism and entrance fee to a tourist attraction (Expenses incurred on or after 1st March 2020 until 31st December 2021) Registered accomodation premises can be check thru link of : http://www.motac.gov.my/en/check/registered-hotel |

1,000 (Restricted) |

| 26 | Additional lifestyle tax relief related to sports activity expended by that individual for the following: Purchase of sport equipment for any sports activity as defined under the Sport Development Act 1997 (excluding motorized two-wheel bicycles); Payment of rental or entrance fee to any sports facility; and Payment of registration fee for any sports competition where the organizer is approved and licensed by the Commissioner of Sports under the Sport Development Act 1997. |

500 (Restricted) |

Source: Inland Revenue Board of Malaysia / Lembaga Hasil dalam Negeri Malaysia